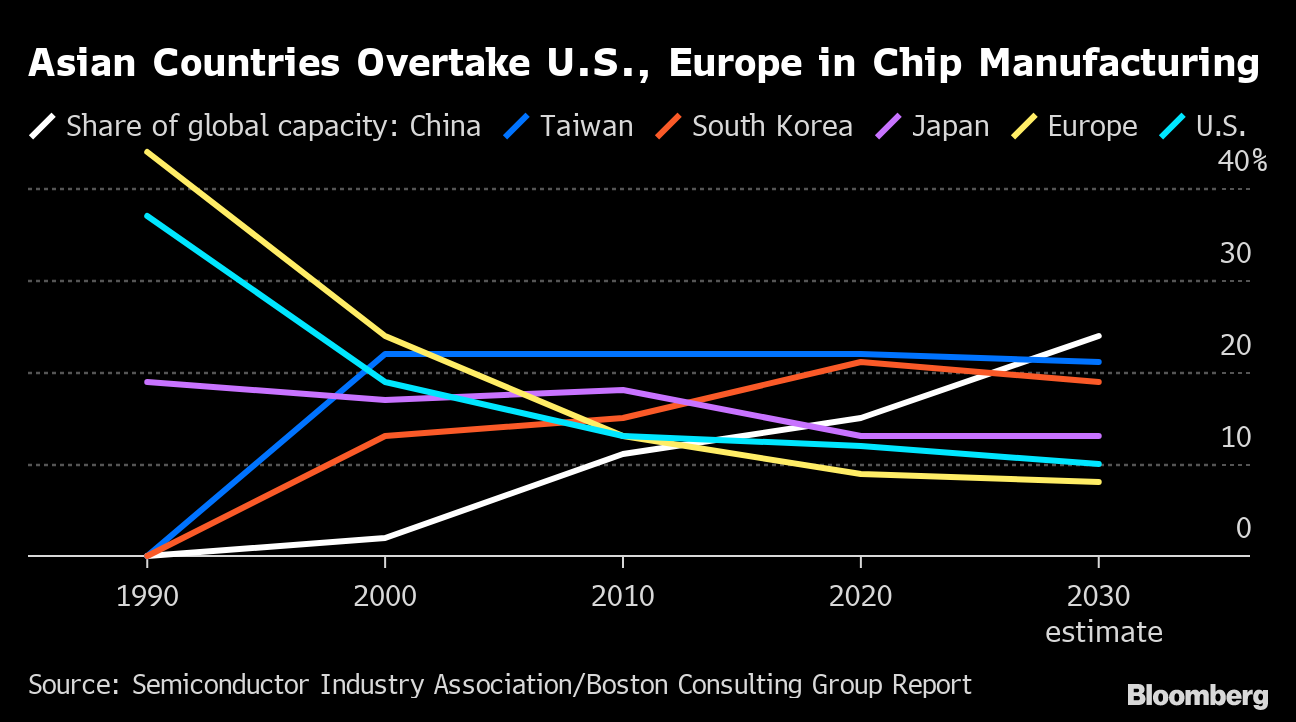

We are witnessing a big production capacity #localization drive by companies in #semiconductor industry recently to avoid new export controls & tariffs under the impact of #geopolitics. To adjust to this, companies will need to rethink their manufacturing & logistics, supply chain partners, warehouse & factory locations, volume targets etc. While this needs massive investments & govts. are offering financial assistance, it’ll take a lot more than money & certainly a lot of time.

It’s a capital intensive game with constant downward price pressures & rising operating costs. For instance, govt. subsidies can help reduce upfront burden for #wafer #fabs & #OSATs but with relatively higher manpower involvement & running costs, the complexity can be much higher for #packaging businesses than fabs. The economics of setting up a fully localized base in a particular region remains a debate.

Though #automation, efficiency improvements, cost down initiatives & clever negotiations with customers can provide some working solutions. Countries/ regions that can facilitate high automation levels & complement with availability of #technical #talent by focusing on #upskilling of people are likely to make a better compelling case for more businesses to consider this localization proposition.